AllCom Credit Union was proud to host another unforgettable Member Appreciation Day, and we’re still smiling from all the fun! The event was a wonderful opportunity to connect with our incredible members — the heart of our credit union — and say thank you for your continued support and loyalty.

From sizzling hot dogs and fresh popcorn to friendly faces and festive vibes, the day was packed with food, fun, and community spirit. It was great to see so many members stop by, share a laugh, and enjoy a well-deserved celebration.

We’re especially grateful to everyone who took part in this year’s giveaway! Congratulations to the lucky winner of the Emeril Lagasse XL French Door Air Fryer Toaster Oven Combo — we hope it brings plenty of delicious meals your way.

Thank you again for being part of the AllCom family. We truly appreciate the trust you place in us and look forward to serving you for many years to come!

Join us for AllCom Member Appreciation Day, where we celebrate the BEST members who make our community thrive!

Hot Dogs | Fun | Friends | Popcorn

WHEN: Saturday, June 21, 2025 9 am – 1 pm

WHERE: AllCom Credit Union 36 Park Ave, Worcester

*No purchase necessary to enter. Must be 18 years or older to enter, open to US entries only. AllCom staff, board members and affiliates are not eligible to enter. One entry per person. Entries must be submitted in-person 6/21/2025 by 12:45 pm. Winner will be announced 6/21/2025 by 1:00 pm and contacted via phone if no longer present at the event. Odds of winning is dependent upon number of completed entries received. AllCom Credit Union is not responsible for misdirected or incomplete entries. This giveaway is sponsored by AllCom Credit Union. For a full set of rules, please contact AllCom Credit Union at 36 Park Avenue, Worcester, MA 01609. VOID WHERE PROHIBITED BY LAW.

If you’re looking for a financial institution that feels more like a neighbor than a number, look no further than AllCom Credit Union. Located on Park Ave. in Worcester, AllCom is where members are known by name, not account number. You’ll always reach a real person when you call, not a recording.

With over 4,000 members and $80 million in assets, AllCom is one of the city’s best-kept secrets. Founded in 1922 to serve employees of the New England Telephone Company, we’ve proudly called Worcester home for more than 100 years. Since 1988, our branch on Park Ave – right across from Starbucks and New England Roast Beef – has been a neighborhood landmark.

But we’re more than just a building on Park Avenue – we’re part of the community. Over the years, we’ve proudly supported and participated in local events, school programs, and charitable initiatives. Whether it’s sponsoring local fundraisers or volunteering at community events, AllCom is woven into the fabric of Worcester life.

Thanks to investments in technology, our members enjoy the same conveniences as they would at a larger bank – from a convenient mobile app to a paperless loan application process – all backed by a team that truly cares.

“Credit Unions are owned by their members and at AllCom, our members come first,” says Laura Ybarra, President & CEO of AllCom since 2022. A Worcester native, Laura’s story is deeply tied to the Credit Union. She joined through a Worcester Public Schools school-to-work program at Doherty High School and has been with AllCom for over 27 years. Her journey from student intern to President/CEO reflects the values we hold dear: loyalty, community, and personal growth.

AllCom serves a broad local membership – from local telephone, gas, utility and postal service employees to individuals and families throughout Worcester County and parts of Middlesex County. If you live, work, or go to school in the area, you’re eligible to join our Credit Union family.

We may be smaller in size, but we think that’s part of our charm. With just one branch and a committed team, we offer a level of personalized service that’s not commonly found. “We carry the same products and offer the same services as larger Banks and Credit Unions,” says Ybarra. That includes standout offerings like The Rate Improver Mortgage, a 30-year fixed mortgage that allows members to lower their rate within 5 years as market rates drop, without refinancing fees.

And while we’re proud to be your local Credit Union, we’re here for you wherever life takes you. Through our partnership with the CO-OP Shared Branch Network, members can access account services at more than 5,600 Credit Unions nationwide. So whether you’re away at college, traveling out of state, or relocating, AllCom goes with you.

At AllCom Credit Union, we’re not just in your neighborhood – we’re part of it. Banking Made Better. Learn more at allcomcu.org.

Simple tips to help you stretch your dollars further.

At AllCom Credit Union, we know that saving money doesn’t always require big changes—it’s the small, everyday habits that can make a big difference over time. Here are a few smart life hacks to help you keep more money in your pocket:

1. Automate Your Savings Set up automatic transfers from your checking to your savings account—even a small weekly amount adds up fast. Out of sight, out of mind, and into savings!

2. Meal Prep Like a Pro Plan meals for the week, shop with a list, and cook in batches. You’ll save money by avoiding takeout and reduce food waste.

3. Use Cashback & Coupon Apps Download apps like Rakuten, Ibotta, or Honey to earn cash back and find coupon codes for everyday purchases, from groceries to online shopping.

4. Cancel Unused Subscriptions Take a few minutes to review your subscriptions and cancel any you don’t use. Those small monthly charges can quietly add up over time.

5. Brew Your Own Coffee We’re not saying skip your morning pick-me-up—just try making it at home. A daily coffee shop run could be costing you over $1,000 a year!

6. Review Your Bills Annually Call your service providers—like internet, cell, or insurance—and ask if better rates are available. Loyalty doesn’t always mean you’re getting the best deal.

Smart money habits start small, but they can lead to big savings. Need help setting up a savings plan or want to explore budgeting tools? Our team at AllCom Credit Union is here to help!

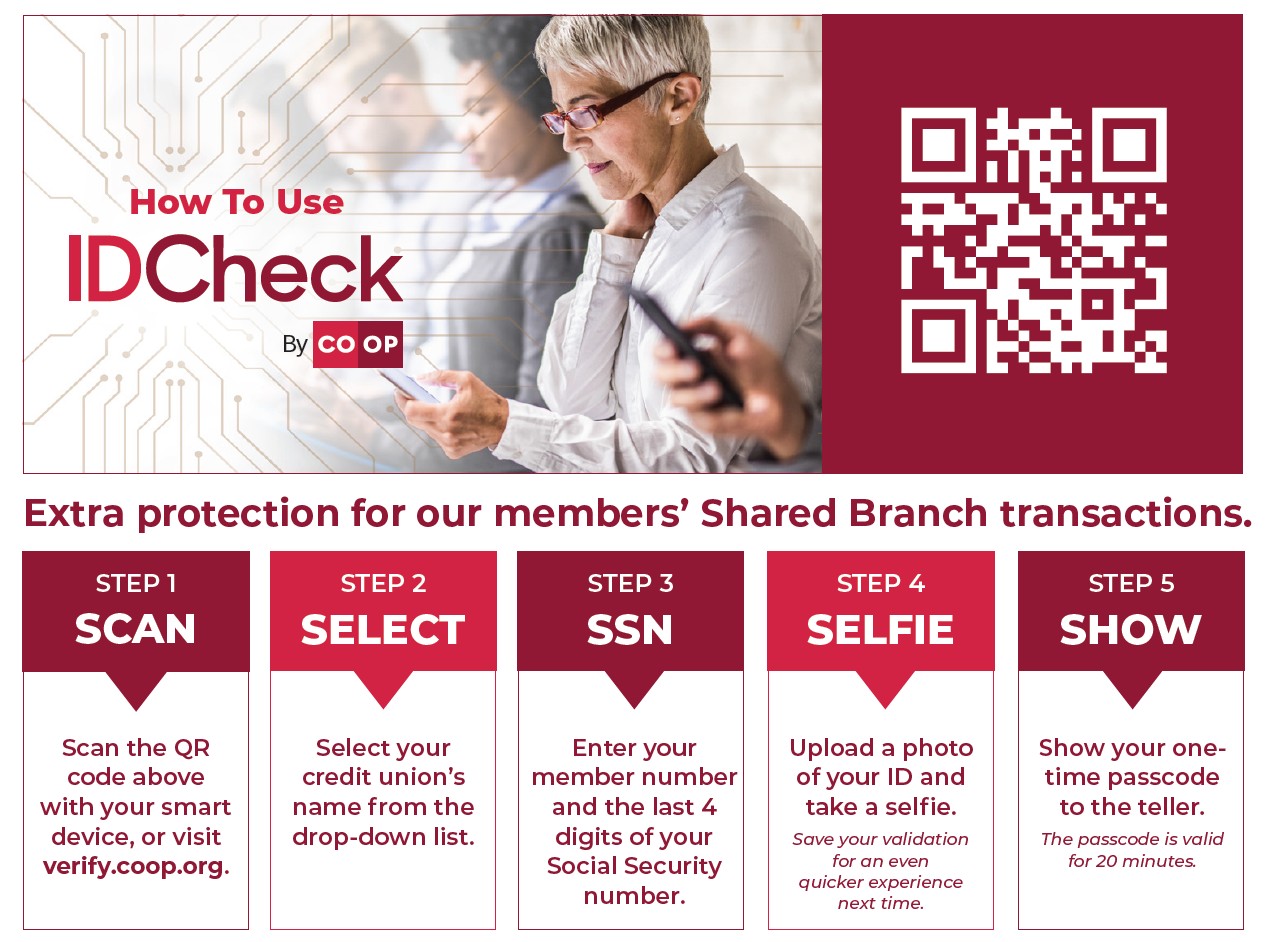

To help prevent account takeover fraud, AllCom is introducing a new ID verification step at Shared Branch locations.

Starting May 1st, if you visit a Shared Branch and present an ID from a different state than the one you’re in, you’ll be asked to complete a quick, one-time verification using a QR code and passcode before making a withdrawal.

This extra layer of security ensures it’s really you accessing your account — not someone pretending to be.

We want to make you aware of an ongoing scam targeting AllCom Credit Union members. Some members have reported receiving phone calls or text messages from fraudsters pretending to be AllCom representatives.

These scammers may ask for sensitive information, such as your credit or debit card number, one-time passwords, or online banking login credentials.

We want to emphasize that our credit union will NEVER call you and ask for confidential information such as your account or card number, one-time passwords, PIN, or password over the phone. If you receive a call requesting this information, even if the caller ID appears to be from our institution, please hang up immediately and call us directly at the number you know to be correct, 888.754.9980.

Your security is our top priority, and we are committed to taking proactive measures to safeguard your personal and financial information. If you have any questions or concerns regarding this matter, please do not hesitate to contact us.

Keeping your contact details current ensures you can fully benefit from AllCom Credit Union’s services and stay informed about important updates. Plus, outdated information could mean missing a critical email or advisory.

Here are three key reasons to update your contact information today:

Enhanced Fraud Protection:

With the rise in online transactions and card-not-present purchases, fraudsters are always looking for vulnerabilities. Providing AllCom with your updated contact details helps us alert you quickly about any suspicious activity and take swift action to protect your accounts.

Secure Delivery of Confidential Information:

A USPS change of address doesn’t guarantee that your account statements or other sensitive documents will be forwarded. Ensure your financial information stays confidential by updating your contact information directly with us.

Stay Informed:

Don’t miss out on important updates, reminders, and time-sensitive notifications—especially if you’ve gone paperless. Keeping your contact information up to date ensures we can always reach you when it matters most.

Updating is quick and easy! Visit us in person or give us a call at 888-754-9980 to make sure we have your latest information.

We’re always working to improve your digital banking experience, and we’re excited to share the latest updates! As of Tuesday, November 5, our digital banking platform has received some fantastic enhancements designed to make managing your finances even easier.

Here’s what’s new:

Username Masking: Your username is now more secure on mobile, showing only the first 4 characters.

Password Visibility Toggle: View your password as you type on both mobile and online platforms for added convenience.

Improved Member-to-Member Transfers: Select prefixes from a dropdown menu instead of typing them manually, simplifying transfers.

Auto-Prompt for Biometrics: Enable biometric login easily by heading to your settings.

Quick Balance: Check your account balances without logging in by enabling this feature in your settings.

Members will notice these changes the first time they log in after updating their app.

Update your app today and explore these new tools designed with you in mind!

AllCom Credit Union members must stay alert to the latest attempts by scammers to access personal financial data. Fraudsters are spoofing email addresses and phone numbers to make it appear as though they are from a trusted source, such as our credit union, government agencies, or legitimate businesses.

Some of our members have recently received emails, text messages, and phone calls from cyberthieves posing as credit union employees, using pieces of personally identifiable information to gain member trust before stealing account funds.

AllCom Credit Union will NEVER ask you for a one-time PIN or any personal passwords!

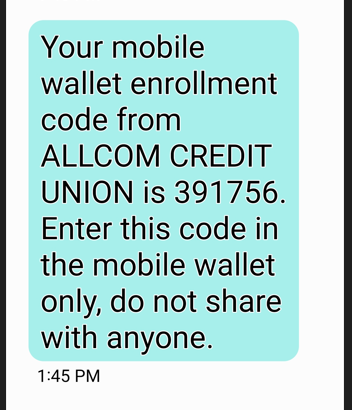

Below shows what a digital wallet text from AllCom may look like. Please note where it says do not share with anyone. This code should ONLY be entered directly into your device when adding cards to your digital wallet. Providing this code to someone pretending to be from AllCom allows the scammer to add your credit/debit card to their mobile wallet. They are then able to start completing transactions immediately.

We want to emphasize that our credit union will NEVER call you and ask for confidential information such as your account number, one-time passwords, PIN, or password over the phone. If you receive a call requesting this information, even if the caller ID appears to be from our institution, please hang up immediately and call us directly at the number you know to be correct (888.754.9980).

Your security is our top priority, and we are committed to taking proactive measures to safeguard your personal and financial information. If you have any questions or concerns regarding this matter, please do not hesitate to contact us.

The new year often comes with the tradition of formalizing goals for the coming months. In a study by Forbes, 38% of adults surveyed said their top New Year’s resolution was improving their finances. This stat comes as no surprise, as financial goals are often tangentially tied to many other aspirations on our list.

Let’s dive into some financial New Year’s resolutions that are easy to achieve and stick to for the long haul!

Build a budget that prioritizes savings

If you’re part of the 38% of Americans prioritizing saving this year, you should know a few key things before you start. First, keep your goal attainable!

The best way to keep your savings resolution is to automate it. Start by picking a budget that prioritizes saving first. The zero-balance budget is a method of managing money where every single penny of your paycheck is accounted for. This type of budgeting lets you consistently automate your savings on payday.

Step up your retirement contributions

If the start of the new year also means performance reviews at your workplace, this goal is easy to tackle! Retirement savings is one of the most important long-term financial goals you can work toward.

Experts recommend increasing your 401(k) contributions by at least 1% annually. If you receive a 3% raise, try increasing your retirement contributions by 1%. You’ll still be getting a 2% raise every paycheck and setting yourself up for success to live a comfortable life when you retire.

Commit to improving your credit score

Have you ever taken a deep dive into your credit report to see if everything is correct? If you answered no, this is your year to familiarize yourself and better understand what impacts your credit score.

It’s essential to know more than just your credit score. Monitoring your credit report once a year will bring you peace of mind and help you spot any potential fraud issues before they spiral out of hand. Remember, you can access one free credit report—which includes your FICO (Fair Isaac Corporation) score—every year at freecreditscore.com.

Assess your finances for extra saving opportunities

Saving more than you already are can sometimes feel like a stretch. Assessing your monthly spending habits can uncover extra saving opportunities you may not even realize you had!

Make extra payments to eliminate debt

Do any of your financial resolutions involve paying down debt faster? Commit to putting “extra” money that comes your way to paying down student loans, credit card debt or your mortgage. Prioritize paying off the debt with the highest interest rates first.