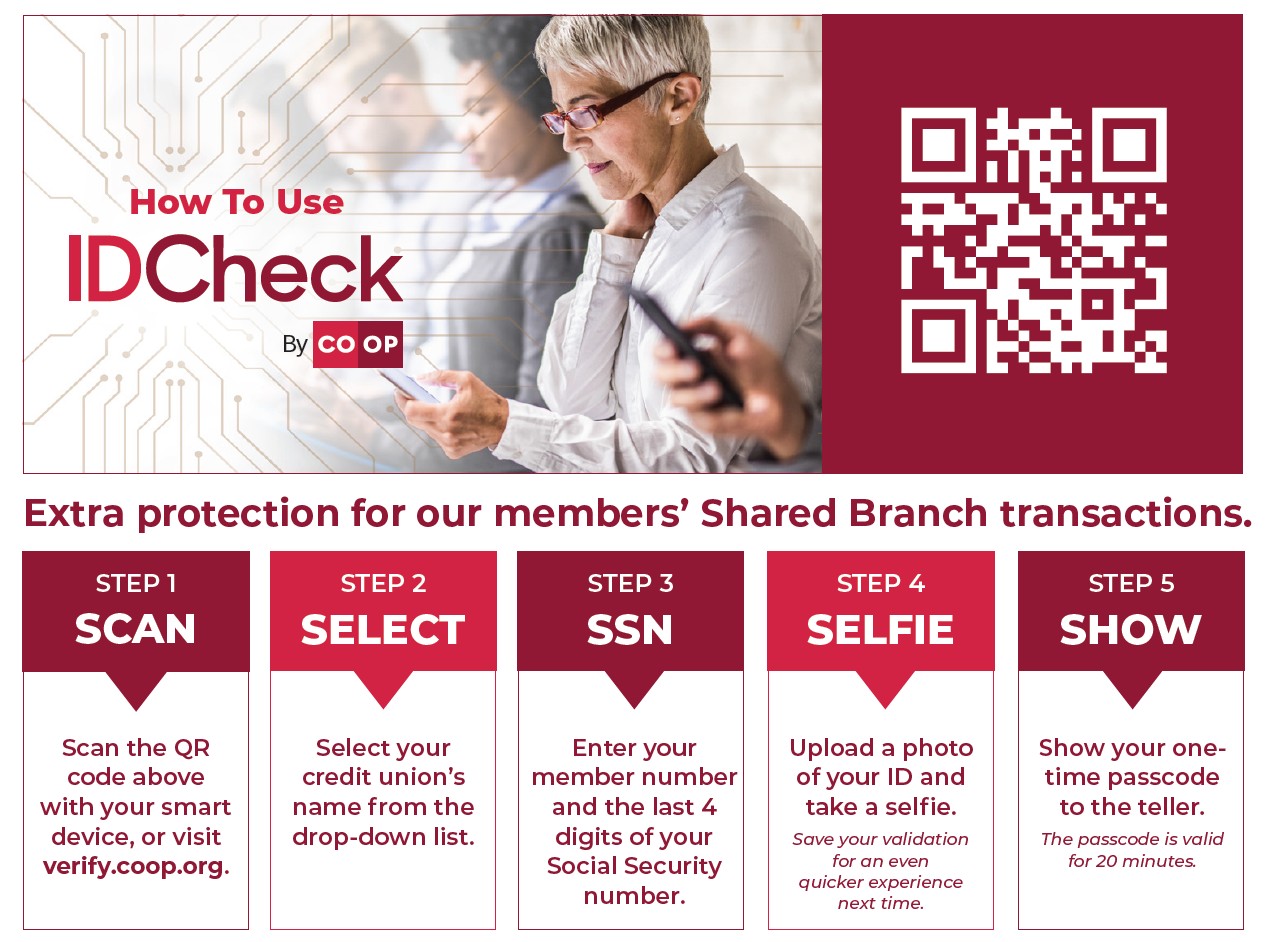

Each year, Americans complete transactions more and more online. Consumers need to stay diligent to prevent becoming a victim of fraud and identity theft.

Here is a list of things you can do right now to make your accounts more secure. There are more tips outside this list but with many things in life, it’s about taking the first step!

Change your passwords so they’re unique and strong

Take the time to start changing your passwords so that each account has a different password. Begin with your most important accounts such as your financial accounts.

The Federal Trade Commission (FTC) provides a great example of a creative password, “Think of a special phrase and use the first letter of each word as your password. Substitute numbers for some words or letters. For example, ‘I want to see the Pacific Ocean’ could become 1W2CtPo!”.

This is an excellent example because it:

- Has upper and lowercase letters

- Contains special characters

- Doesn’t contain personal information

- Is at least six characters long (but ideally could be longer)

- Is memorable to you but gibberish to others

Brainstorm how you can make every password memorable but different. If you have trouble remembering your passwords, consider a password manager.

Update your usernames so they’re unique too

It’s best to vary your login credentials to ensure that each financial account has a unique username and a unique password. Why? If you created a username and password that was the same as the one you had during a breach, your other financial accounts could have been compromised as well.

Sometimes apps require an email for your username. It’s not ideal because you cannot make it unique. Think about having an email for purchases and services you want to try and another email account for important communications. It can help with spam but also may limit your chances of exposure through your email.

Sign up for two-factor authentication

Two-factor authentication is key in securing your financial info. Here’s how it works: After logging in to your credit union’s online or mobile banking, you’ll get a code via text or email. The password and code can confirm that the member is the only one who is accessing their account.

Two-factor authentication is more secure than security questions. Your answers to security questions can sometimes be found on social media. For example, your mother’s maiden name or your favorite activity could be found if you posted about either.

Plus, it’s easy to forget how you answered a question. Two-factor authentication can make your life a little easier and safer. If you haven’t already, sign up for two-factor authentication where you can.

Opt in to automated account alerts

Sign up for automated alerts to help protect yourself from fraud. It takes just a few minutes and you can customize the alerts. With alerts set up, if you didn’t make a transaction, you can see it right away and contact your financial institution.

Install antivirus and get a VPN

Any device is vulnerable to hackers, including your smartphone. Install an antivirus that protects against malware, ransomware or trojan horses.

Also get a VPN, which encrypts your traffic, and use it anytime you’re online. Both an antivirus and VPN are worth the annual fee.

Say no to public Wi-Fi

When you’re getting work done at a coffee shop or browsing your phone at the airport, it is very tempting to hop on to the free public Wi-Fi. Don’t do it!

There are a few ways hackers can easily steal your information on public Wi-Fi:

- Fake Wi-Fi connections are simple to create and allow fraudsters to access your private information. Should you join Joe’s Coffee or Joe’s Coffee Shop? Both could be accurate but one could be malicious.

- Packet sniffing is when a hacker can scan everyone’s information on public Wi-Fi with easy to use, free software. Almost anyone can find your passwords.

- Sidejacking is when a hacker can access anywhere you’re logged in at the time. From there, they can download malware among other things.

Start paying with your smartphone

Mobile wallets such as Apple Pay, Google Pay or Samsung Pay help keep your transactions safe by creating a unique code for each transaction. It’s more secure than swiping because the store doesn’t have your name, card number or security code. All of that information stays private.

Add your debit and credit card to your mobile device and use it for any of your in-person payments. Hundreds of thousands of stores accept digital wallets so try it on your next trip to the store.